Stocks saw an increase as hopes grew that inflation pressures would ease, according to the latest market update. The S&P 500 rebounded after a two-day decline, and traders anticipate the implementation of the “T+1” rule, which will shorten the settlement time for US equities. Meanwhile, Treasury yields remained stable after Fed Governor Christopher Waller expressed his belief that the neutral interest rate is still relatively low. However, he cautioned that excessive fiscal spending could potentially impact this trend. Additionally, Wall Street found some relief in the University of Michigan’s data, which showed that consumers now expect prices to rise at a slightly lower annual rate of 3.3%.

According to Jeff Roach at LPL Financial, upon further examination, consumers are not as negative about the trajectory of inflation. This could lead to a slowdown in consumer spending, which would alleviate inflationary pressures from the demand side of the economy.

During a session with low trading volume, the S&P 500 bounced back and reached the 5,300 level, recovering from the losses earlier this week. The Nasdaq 100 reached a new all-time high, driven by the gains in Nvidia Corp. and Apple Inc. Additionally, cryptocurrency stocks saw an increase as the Securities and Exchange Commission paved the way for the future launch of the first US exchange-traded funds that invest directly in Ether.

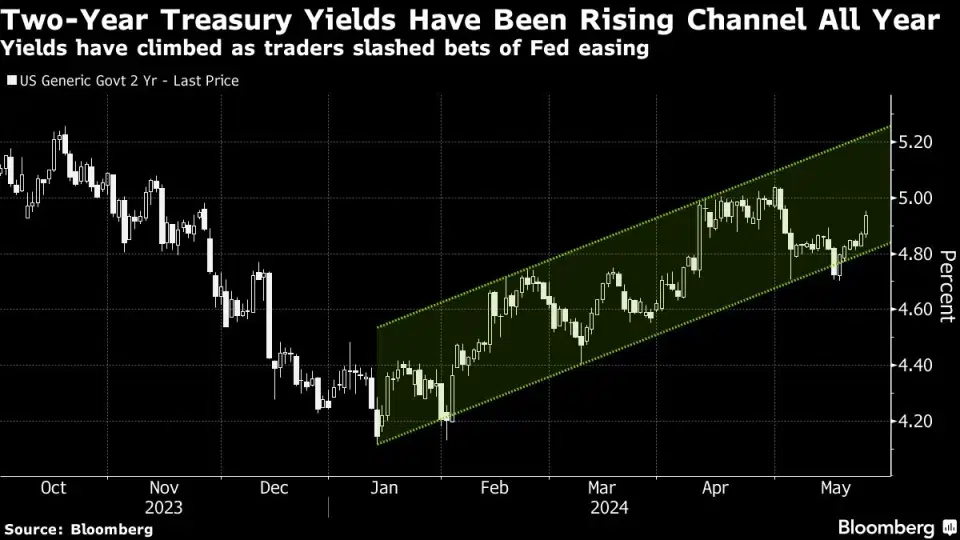

US 10-year yields dropped by one basis point to 4.46%, as the bond market closed early in anticipation of the Memorial Day holiday. The dollar ended its four-day winning streak, while the yen fluctuated due to Japan’s currency official reiterating their commitment to taking action against excessive currency movements. Oil and gold saw slight increases.

According to Jim Baird at Plante Moran Financial Advisors, the consumer outlook weakened in May due to concerns about the labor market and the possibility of higher interest rates for a longer period. Baird questioned whether consumers would continue spending or start cutting back in anticipation of tougher times ahead. If May’s sentiment index is any indication, consumers are likely to be more pessimistic and tighten their spending in the coming months.

Stuart Paul at Bloomberg Economics expects the Fed’s preferred inflation measure, the core PCE deflator, to moderate to its slowest pace so far this year. However, this moderation is likely due to a significant decrease in airfares, while inflation continues to be supported by easing financial conditions.

According to Quincy Krosby at LPL Financial, if the data comes in lower than expected, the report could have a positive impact on the market. However, even if the Personal Consumption Expenditures (PCE) remains stable, investors may still be satisfied that inflation is somewhat under control. Nevertheless, recent market activity suggests that both investors and traders are becoming impatient with the Federal Reserve’s inability to control rising prices.

The minutes from the Federal Open Market Committee meeting held on May 1, which were released on Wednesday, revealed that while participants believed that monetary policy was in a good position, some officials expressed a willingness to tighten further if necessary.

Economists from Goldman Sachs Group Inc., including Jan Hatzius, have revised their forecast for the first rate cut by the Fed from July to September.

In our previous report, we highlighted that comments from Federal Reserve officials indicated that a rate cut in July would require not only improved inflation figures but also significant signs of weakness in economic activity or labor market data. Florian Ielpo from Lombard Odier Asset Management observes that the week was once again dominated by concerns about the Fed’s actions. He also reminds us that despite the rising interest rates, company earnings have remained strong, implying that the impact of positive economic news may not be as straightforward as expected. Ryan Grabinski from Strategas Securities further notes that mentions of inflation during S&P 500 company earnings calls have declined, mirroring the actual trend in inflation.

Deutsche Bank AG’s Binky Chadha believes that the stock market can continue to reach new highs, even if the Federal Reserve does not lower interest rates this year. This is because the economy and corporate earnings are still growing.

On the other hand, Bank of America Corp. strategist Michael Hartnett warns that the global equity market rally may be overheating. He suggests that the increasing breadth of the market could be a contrarian sell signal.

Ross Mayfield from Baird Private Wealth Management points out that while concentrated markets have not historically resulted in poor returns, a broader market is typically a sign of a stronger economy.

“As the market has expanded significantly in recent months, concerns over the heavy concentration in Big Tech stocks have diminished,” he observed.

In a bullish market characterized by stability, cautious investors are grappling with the challenge of finding effective strategies to hedge their positions.

Traditional methods such as purchasing put options, which have historically served as a means of protecting against downturns, have failed to yield positive results for investors who remain wary of the ongoing rally that has propelled global stocks to new record highs.

Volatility sellers have pushed the VIX Index to its lowest level since 2019 this month, and the S&P 500 Index has gone over 300 days without experiencing a single-session drop of 2% or more.

Corporate Highlights:

The leading US auto-safety regulator has expanded its investigation into Waymo, the autonomous-vehicle subsidiary of Alphabet Inc., following the identification of additional incidents involving collisions or potential violations of traffic laws by the company’s vehicles.

- Workday Inc. saw a decline in its stock price as the company revised its full-year forecast for subscription revenue, citing cautious customer behavior.

- SpaceX, led by Elon Musk, is reportedly in discussions to sell shares at a price that could value the company at around $200 billion.

- Waystar Holding Corp., a healthcare payments software firm, is moving forward with its planned initial public offering in the US, expected to launch on Tuesday.

- Eli Lilly & Co. will invest $5.3 billion to increase production of a key ingredient in its weight-loss and diabetes shots, responding to high demand and shortages.

- Novo Nordisk A/S’s diabetes drug Ozempic showed promising results in reducing the risk of death in a kidney-disease study, adding to its growing potential in treating various disorders.

At 4 p.m. New York time, the S&P 500 index increased by 0.7%, while the Nasdaq 100 index rose by 1%. However, the Dow Jones Industrial Average remained relatively stable. The MSCI World Index also experienced a 0.5% increase.

In the currency market, the Bloomberg Dollar Spot Index dropped by 0.2%. The euro saw a 0.3% rise against the dollar, reaching $1.0849. Similarly, the British pound also increased by 0.3% against the dollar, reaching $1.2740. On the other hand, the Japanese yen remained unchanged at 156.93 per dollar.

Moving on to cryptocurrencies, Bitcoin witnessed a 2.1% surge, reaching $69,175.88. However, Ether experienced a slight decline of 0.3%, reaching $3,746.38.

In the bond market, the yield on 10-year Treasuries decreased by one basis point to 4.46%. Similarly, Germany’s 10-year yield also declined by one basis point to 2.58%. Conversely, Britain’s 10-year yield remained relatively stable at 4.26%.

In the commodities market, West Texas Intermediate crude oil rose by 1.1%, reaching $77.75 per barrel. Spot gold also experienced a 0.2% increase, reaching $2,334.41 per ounce.

Please note that this story was created with the assistance of Bloomberg Automation, and additional assistance was provided by Alexandra Semenova, Sagarika Jaisinghani, Jan-Patrick Barnert, and Vince Golle.