Asian stocks fell as concerns about the US economy overshadowed hopes for early Federal Reserve policy easing. Shares in Japan and South Korea declined, while those in Hong Kong and mainland China experienced fluctuations. US equities futures remained stable.

In Asia, Treasury yields stabilized after a rise on Monday triggered by data showing a faster contraction in US factory activity. The 10-year yields increased by two basis points to 4.41%, following a previous decrease of 11 basis points. Australia’s equivalent yield dropped by five basis points, while New Zealand’s slipped by eight basis points.

The dollar, which had weakened against most of its Group-of-10 counterparts earlier, stabilized. Asian currencies like the Thai baht and Malaysian ringgit strengthened.

The latest US data reveals that the manufacturing sector is facing challenges in gaining momentum. This is mainly due to high borrowing costs, limited investment in equipment, and a decrease in consumer spending. Additionally, manufacturers are also struggling with increased input costs.

Gary Pzegeo from CIBC Private Wealth US commented on the Manufacturing ISM data, stating that it confirms the prevailing economic trends of slower growth, decelerating inflation, and a tight labor market. Pzegeo also mentioned that there is an increased likelihood of a rate cut later this year, which is reflected in the pricing of interest rate futures.

Swap contracts tied to upcoming meetings continue to fully expect a quarter-point rate cut in December. The probability of a rate cut in September has risen to around 50%, with high odds also given for a rate cut in November.

Ian Lyngen and Vail Hartman from BMO Capital Markets noted that there have been some signs of weakness in the real economy, particularly in consumption. As a result, investors are cautious and monitoring for any indications that the downward trajectory is accelerating.

The S&P 500 index experienced a late surge as a rally in big tech companies offset a sharp decline in energy producers. The New York Stock Exchange faced technical issues earlier in the day, leading to temporary halts in trading due to erroneous volatility.

In the commodities market, oil prices dropped as OPEC+ announced plans to increase production. Meanwhile, Bitcoin briefly reached a record high of $70,000, and gold maintained its strongest gain in two weeks following weak US economic data, which raised expectations of a rate cut by the Federal Reserve.

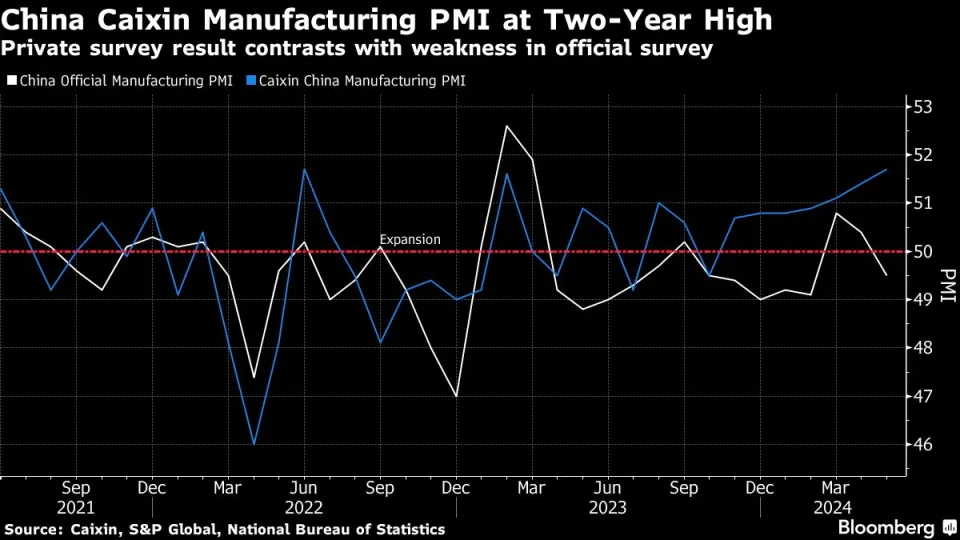

In Asia, two data releases from China on Monday provided some optimism for the country’s sluggish economy. Shanghai and Shenzhen saw an improvement in homebuyer sentiment after easing property restrictions, signaling a positive development for the struggling real estate sector after months of decline.

Additionally, a recent private survey revealed that China’s manufacturing sector experienced its fastest expansion in almost two years in May. This contradicts the weak official data that had previously dampened the country’s growth prospects.

Furthermore, investors are eagerly awaiting the results of India’s elections on Tuesday. Exit polls indicate that Prime Minister Narendra Modi is likely to secure a third term victory.

As the US earnings season draws to a close, traders are now turning their attention to the trajectory of inflation. They are particularly interested in whether inflation is cooling off or if it remains stuck in a loop that would prolong the current state of “higher-for-longer” interest rates. Chris Larkin from E*Trade at Morgan Stanley emphasizes that the upcoming jobs report will serve as a crucial test in this regard.

In addition to the jobs report, traders will also closely monitor a series of labor-market indicators throughout the week, with particular focus on Friday’s payrolls figures.

Oscar Munoz, from TD Securities, stated that if job openings continue to decline this week, it will further emphasize that the labor market is no longer a significant concern for inflation in the near future.